Ugh, ugh, ugh. This makes me so mad.

Ugh, ugh, ugh. This makes me so mad.

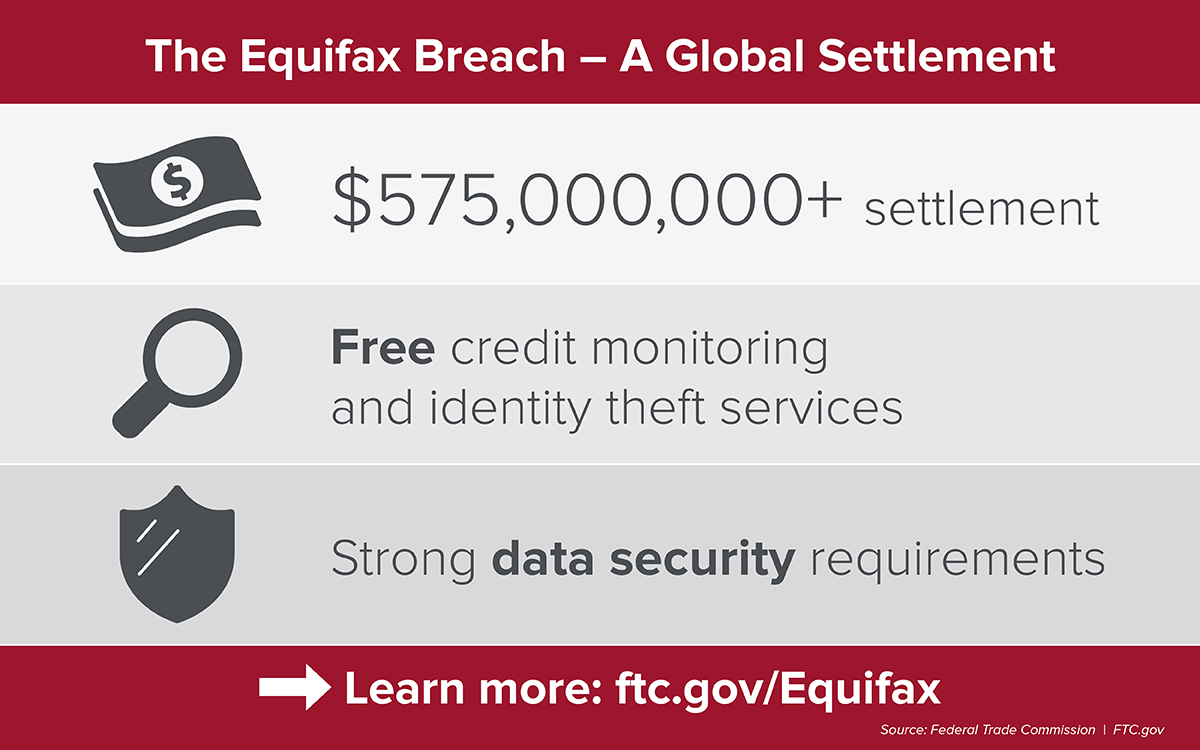

So, last week, I shared with you all the information from the FTC information about the Equifax settlement for those of us who were affected by their data breach last year.

As you may recall, Equifax offered either up to 10 years of credit monitoring (plus assistance with dealing with any identity theft claims as a result of their breach) OR $125 per person.

The fine print said that the $125 was for folks who already had credit monitoring, but – duh! – a lot of people opted for the cold, hard cash. And the claim “went through”. Or so it looked like on the website.

Well, last night, Equifax apparently took out a calculator and realized that the $33 million that they had set aside to cover this massive breach of our data – and the public trust – wasn’t going to be enough to cover all the folks asking for their $125 payout.

(The math never worked, to be honest, considering that over 145 million people were affected!)

Now, Equifax is saying “Aw shucks, we’re not going to have enough money to pay everyone $125 after all.” The FTC has even updated their press release to say:

Previously, a cash payment was identified as an option, but there are limited funds available.

If you requested the $125 option after hearing about this settlement – either on KOAB or elsewhere – you probably already know this…

Because apparently Equifax is now emailing folks and encouraging them to reconsider and opt in instead for the credit monitoring.

And, oh, by the way, if you decide to stick with the cash payout, then FYI, it won’t be $125. Equifax is now saying that they are going to reduce the amount – probably by a whole lot.

Talk about kicking us when we’re down. This is the opposite of repairing the trust breach.

I’d sure like to know (a) who their accountants are (because get a new calculator!) and (b) who their PR people are (because they are going to need to look for a new job!).

Anyone else find this super maddening?

Leave a Comment